Insurance is a contractual arrangement in which an individual or entity, known as the policyholder, pays regular premiums to an insurance company in exchange for financial protection against specified risks or losses. Here is an overall outline of how protection functions:

- Identifying Risks:

Insurance work is designed to protect against risks or potential losses. These risks can vary depending on the type of insurance, such as health, auto, home, life, or business insurance. The policyholder assesses the risks they want to protect against and selects the appropriate insurance coverage.

- Choosing an Insurance Policy:

Once the risks are identified, the policyholder selects an insurance policy that matches their needs. Insurance companies offer various types of policies with different coverage options, deductibles, limits, and premiums. The policyholder reviews the terms and conditions of the policy and agrees to pay the premiums.

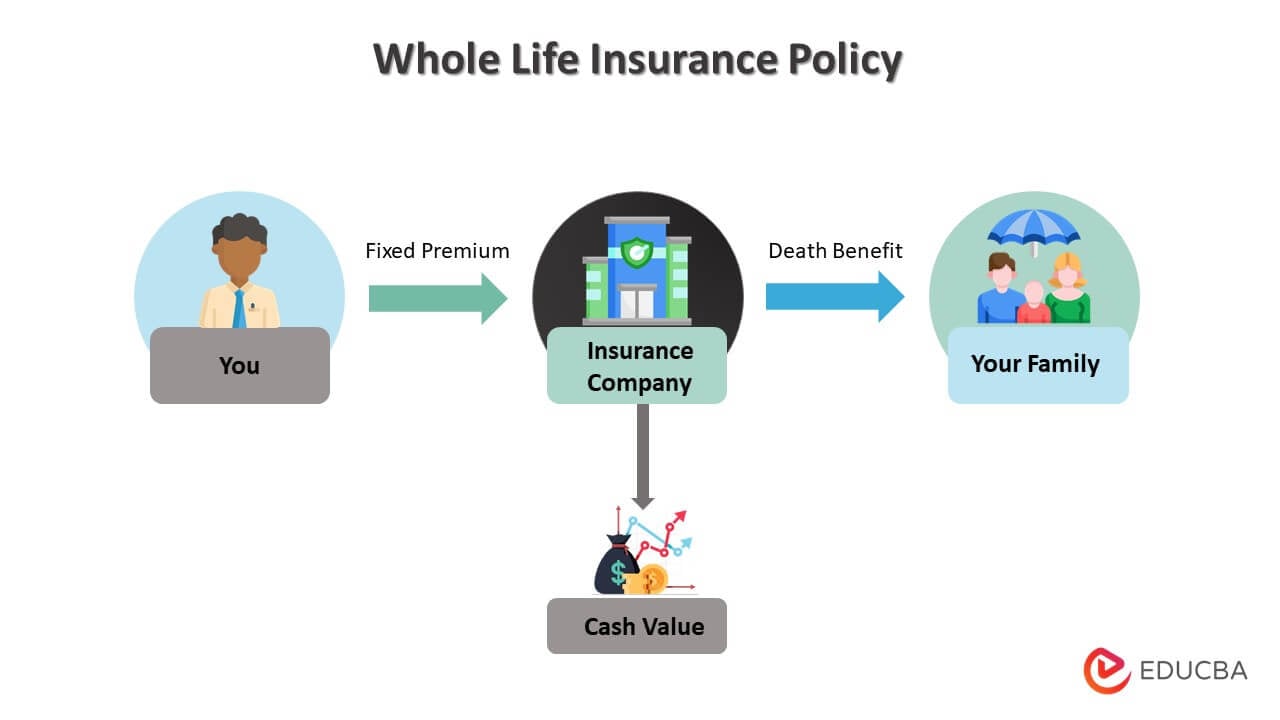

- Premium Installments:

The policyholder pays customary charges to the insurance agency. Premiums are typically paid monthly, quarterly, semi-annually, or annually, depending on the terms of the policy. The amount of the premium is based on various factors such as the type of insurance, coverage amount, risk factors, and the policyholder's personal circumstances.

- Policy Coverage:

Once the policy is in effect and the premiums are paid, the insurance policy provides coverage for the specified risks outlined in the policy. For example, an auto insurance policy may cover damage to the insured vehicle in the event of an accident, or a health insurance policy may cover medical expenses for covered illnesses or injuries.

- Occurrence of a Loss:

If a covered loss or event occurs, the policyholder must notify the insurance company promptly. For example, in the case of an auto accident, the policyholder would contact their auto insurance company and provide the necessary information, such as the date, time, location, and details of the incident.

- Claims Process:

After receiving the notification of a loss, the insurance company initiates the claims process. The policyholder submits a claim, providing documentation and evidence to support the claim. This may include photographs, police reports, medical records, or repair estimates, depending on the nature of the loss.

- Claims Evaluation:

The insurance company assesses the validity of the claim and reviews the policy coverage. They investigate the circumstances surrounding the loss to determine if it falls within the scope of the policy. If the claim is approved, the insurance company pays out the agreed-upon benefits or compensation to the policyholder, subject to any deductibles or limits specified in the policy.

- Policy Renewal:

Insurance policies are typically valid for a specific period, such as one year. Before the policy expires, the insurance company may offer a renewal option. The policyholder can choose to renew the policy by paying the premiums for the next term. The insurance company may adjust the premiums based on factors such as claims history or changes in risk factors.

It's important to note that insurance policies can have specific terms, conditions, exclusions, and limitations that policyholders should be aware of. It's advisable to carefully review the policy documentation and consult with the insurance company or an insurance professional to fully understand the coverage and obligations involved.

- Contact Us

Get the insurance coverage you need with easy and reliable service. We offer comprehensive policies to meet your needs, plus experienced agents to help you every step of the way. Get started now and get peace of mind with Insurance work.

- image source:

https://cdn.educba.com/academy/wp-content/uploads/2022/11/Whole-Life-Insurance-Policy.jpg

{kind=link}

{kind=link}

0 Comments